Most couples don’t fight about “money” in general; they fight about unclear expectations. A budget is simply a shared plan that tells every unit of income where it goes before you spend it. Think of it as a map: income at the top, spending paths below. If you skip the map, each partner drives in their own direction and you crash into overdrafts or hidden debts. Below are practical couples budgeting tips to avoid money mistakes that quietly wreck trust, even in otherwise strong relationships.

Defining the basics: what your joint budget really is

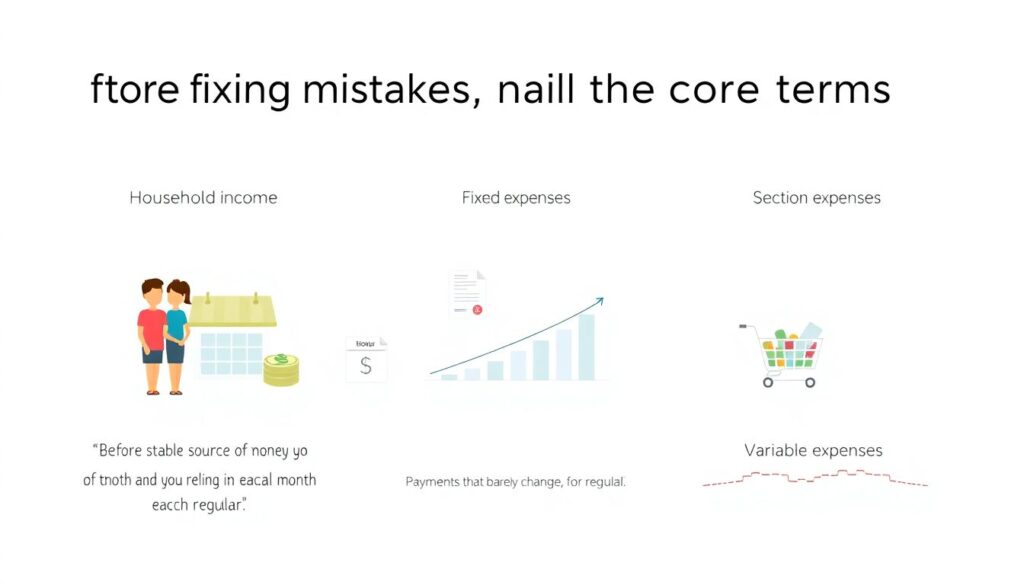

Before fixing mistakes, nail the core terms. “Household income” is every stable source of money you both rely on each month, not just salaries but also bonuses you treat as regular. “Fixed expenses” are payments that barely change: rent, loans, insurance. “Variable expenses” are flexible: groceries, fun, gifts. A “joint budget” is the document (or app) where you assign every dollar of household income into categories. [Diagram: income at the top → split into fixed, variable, savings, debt → leftover equals zero.]

Mistake 1: No shared financial “dashboard”

A huge budgeting error is having no single place where both of you see the full picture. One person tracks things in their head, the other glances at bank notifications, and no one really knows what’s happening. Instead, act like a small startup and build a shared dashboard. It can be a Google Sheet or one of the best budgeting apps for couples to track expenses in real time. [Diagram: two people → one shared dashboard → same numbers → fewer surprises, fewer arguments.]

Individual vs couple budgeting: key differences

Budgeting alone is like playing solo tennis; you only react to your own shots. In a couple, it’s doubles: your choices affect your partner’s side of the court. With solo budgets, irregular spending (gifts, trips, gadgets) is just your problem. In a joint budget, surprise purchases can disrupt rent, daycare, or debt payments. That’s why how to manage finances as a couple without fighting requires extra rules: agree on a “no-questions” personal allowance, define a spending limit that needs a quick check-in, and review big goals together every month.

Mistake 2: Confusing “fair” with “50/50”

Many partners assume “we split everything in half” is automatically fair. Technically, that’s a cost-splitting rule, not a fairness rule. If one partner earns twice as much or carries old student loans, strict 50/50 can silently breed resentment. A more technical alternative is the proportional method: each person covers expenses based on their share of total income. [Diagram: Partner A = 60% of income, B = 40% → each pays the same percentage into joint costs.] This lets the lifestyle match combined income without crushing one person.

Financial planning for couples before marriage

Engaged or just moving in? Financial planning for couples before marriage should feel like a premarital “system check,” not an interrogation. Define three terms clearly: “joint money” (for shared life), “personal money” (for freedom), and “family reserves” (for emergencies). Before signing a lease or booking a big wedding, run a basic stress test: what if one of you loses a job for three months? [Diagram: baseline budget → remove one income → check which expenses must shrink.] If the model collapses instantly, scale commitments back now, not after the honeymoon.

Mistake 3: Budget without goals = numbers without direction

Another trap: building a neat spreadsheet with no real-world targets behind it. Without goals, you’ll keep asking, “Can we afford this?” instead of “Does this help us get where we want?” Define at least three time horizons: short term (next 12 months), medium (1–5 years), and long (5+ years). Link each horizon to exact numbers: pay off 5,000 in debt, build a 3‑month emergency fund, save 20,000 for a home deposit. [Diagram: three columns labeled Now / Soon / Later → each with a dollar target → tied back into budget categories.]

Mistake 4: Ignoring different money personalities

Every couple has some version of “spender vs saver,” but that’s just surface level. Underneath are different risk tolerances, timelines, and definitions of “enough.” Treat these as parameters, not flaws. For instance, one partner might prioritize liquidity (cash on hand), the other long‑term growth (investments). Compare your financial “settings” like tech profiles: low/medium/high risk, short/medium/long horizon. [Diagram: two sliders for each partner → risk level, time horizon → overlapping zone = shared strategy.] Design your budget to fit the overlap, not to force one person to convert the other.

How to actually talk about money without a blow‑up

Knowing how to manage finances as a couple without fighting is mostly about process. Never start budget talks in the middle of a crisis purchase (“Why did you buy that?”). Instead, schedule a recurring “money meeting” with a fixed agenda: check balances, review last month, adjust categories, pick one decision. Keep it to 30–40 minutes. Use neutral language: “The category is over budget” beats “You overspent.” If emotions rise, park the topic, log the issue in your dashboard, and revisit it in the next meeting with data instead of heat.

Mistake 5: Tracking nothing and trusting memory

Relying on “we’ll remember roughly what we spent” is like running a lab without instruments. You need at least three streams of data: automatic bank/credit card feeds, manual cash entries, and snapshots of account balances at month‑end. Compare analog methods (paper envelopes, whiteboard notes) with digital tools (spreadsheets, apps). Analog versions are simple but fragile; they fail when you’re busy or traveling. Digital tools, especially those that sync accounts, reduce manual input and show trends. Use whichever method you’ll both actually sustain for six months straight.

Choosing tools: apps vs spreadsheets vs envelopes

Let’s compare three common systems. Envelopes (physical cash categories) offer strong spending limits you can see, but they’re awkward for online payments. Spreadsheets are highly customizable and transparent; great if one of you enjoys tinkering with formulas. The best budgeting apps for couples to track expenses add syncing, notifications, and auto‑categorization. [Diagram: Envelopes = tactile control; Spreadsheet = flexibility; Apps = automation.] Pick one “primary” tool and stick with it for a quarter; constant switching is its own expensive mistake.

Mistake 6: Treating debt as a background noise

Many couples list debt payments as just another monthly bill without calculating the real cost. Debt has three key parameters: balance, interest rate, and term. Put them in one shared view: which balances are highest, and which interest rates are punishing? [Diagram: bars sorted by interest rate, not balance → tallest bar = debt to attack first.] A practical rule is to keep minimums on all debts, then target either the highest interest (“avalanche”) or the smallest balance (“snowball”) with all extra money. Agree on the method so no one feels ambushed by aggressive payments.

Mistake 7: No emergency buffer for the couple

An emergency fund is not a bonus savings pot; it’s the system’s shock absorber. For a couple, it should sit in a separate, highly liquid account, labeled specifically as “Emergency only.” A realistic target is 3–6 months of core expenses: housing, utilities, basic food, transport, medicine. [Diagram: monthly core cost × 3–6 = target number.] Start with a small milestone, like 1,000, to create quick momentum, then auto‑transfer a percentage of income every payday. Without this buffer, every flat tire or dental bill becomes a budget crisis and, often, an argument.

Mistake 8: One person as the “CFO,” the other in the dark

It’s fine if one partner handles more of the execution—paying bills, updating apps—but it’s dangerous when only one understands the system. If that person gets sick, burned out, or resentful, the entire financial structure collapses. Treat roles like in a project: one “owner,” but joint visibility. Both should know logins, account locations, loan terms, insurance details. [Diagram: central vault of information → two keys, one for each partner.] Review this “map” at least twice a year so no one feels excluded or powerless.

Money management advice for married couples in long‑term mode

Over decades, inflation, kids, career changes, and aging parents will all stress‑test your plan. Good money management advice for married couples is to schedule bigger‑picture reviews at life events: new job, birth of a child, buying a home, or a major health change. In those meetings, update insurance, adjust saving rates, and recheck your risk profile. Think of it as updating your operating system to match new hardware. Keeping the budget alive and aligned with reality is what turns today’s choices into tomorrow’s options instead of tomorrow’s regrets.

Putting it all together: a simple workflow

Wrap everything into a repeatable loop. Step one: define shared goals and money personalities. Step two: choose one main tool and build a joint dashboard. Step three: hold monthly money meetings to review data, tweak categories, and decide on one improvement. Step four: run an annual “audit” of debts, savings, and risks, adjusting your plan like engineers tuning a system. This practical rhythm turns abstract couples budgeting tips to avoid money mistakes into a concrete habit, replacing confusion and blame with clarity and predictable progress for both of you.