Why financing growth is tricky for small businesses

Financing growth sounds simple: you see demand, you add capacity, revenue rises. In practice, the timing, risk and cash‑flow profile rarely line up so neatly. You spend money on marketing, staff, inventory or equipment long before the additional cash starts coming in. That gap is why small business loans for growth, grants, equity and alternative funding exist in the first place. The main challenge is not just “getting money” but matching the structure of the money to how and when your business will realistically earn it back, without suffocating day‑to‑day operations or diluting ownership more than necessary.

Core financing archetypes: debt, equity and hybrids

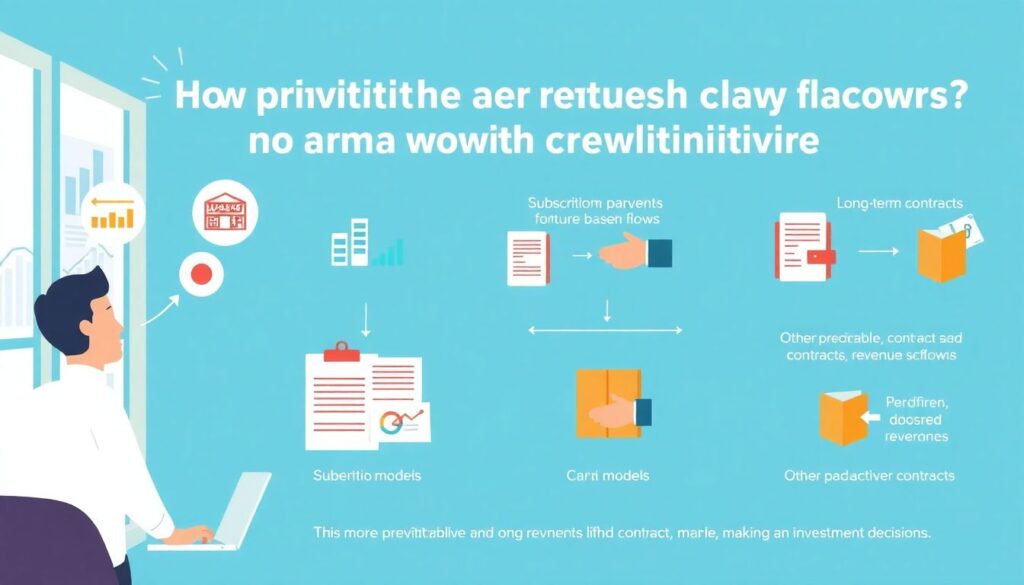

At a high level, all the best financing options for small businesses fall into three buckets: debt, equity and hybrid models. Debt assumes you’ll repay principal plus interest on a schedule, so it works best when cash flows are relatively predictable. Equity assumes investors share in upside and downside through ownership; there are no fixed payments, but you give up part of your company and some control. Hybrid models, like revenue‑based financing or convertible notes, sit in between: they adjust repayments to performance, but still maintain an expected return profile for the capital provider.

Debt-based options: from classic loans to expansion capital

Traditional bank term loans and government‑backed products (like SBA loans in the U.S. or similar schemes elsewhere) remain the backbone of growth financing. These are often branded or structured as small business expansion loans, where a lump sum is used for opening new locations, buying machinery or funding a major product launch. The upside is relatively low cost of capital if your credit is solid, with fixed interest rates and defined maturity. The downside is that lenders underwrite conservatively: they typically require collateral, personal guarantees and historical financials that prove serviceability, which many younger businesses simply don’t have yet.

Within this category, small business loans for growth work especially well for businesses with tangible assets (real estate, vehicles, production equipment) or very stable recurring revenue that can be modeled with confidence. For a restaurant chain adding a second site or a manufacturing firm automating part of its line, term loans can be efficient because the future cash flows from the project are fairly forecastable. However, if your growth plan is more experimental—say a startup testing a new market with highly uncertain conversion rates—the rigidity of fixed amortization schedules can quickly become a strain rather than a support.

Flexible credit: lines, cards and working capital instruments

When growth depends on managing short‑term swings—like stocking up before a seasonal sales spike—flexible credit facilities usually beat long‑term loans. Instruments such as small business lines of credit for growth allow you to draw funds as needed, up to a limit, and pay interest only on what you use. This is ideal for bridging gaps between paying suppliers and collecting from customers. Compared with term loans, lines of credit are better aligned with variable working capital cycles: you can increase orders ahead of a big campaign and then pay down the line as cash comes in.

In parallel, working capital financing for small business can take other forms: invoice factoring, supply‑chain financing, merchant cash advances and business credit cards. Each has a distinct risk‑pricing structure. Factoring shifts credit risk on your receivables to a financier, improving liquidity but at a discount to invoice value. Merchant cash advances monetize future card sales with very high effective APRs, making them suitable only for short‑term, high‑margin opportunities. Credit cards are convenient and often used as a default tool, but revolving expensive balances to fund long‑term assets is financially hazardous, as it mismatches the duration of debt and the economic life of what you’re financing.

Equity and quasi‑equity: trading ownership for acceleration

Equity financing—from angel investors, venture capital funds or strategic partners—solves some of the timing issues of debt by removing mandatory repayments. Instead, investors expect returns through dividends, profit distributions or, more often in high‑growth scenarios, an exit event like an acquisition or IPO. For businesses in innovation‑driven sectors, equity can be the only realistic option because future cash flows are too uncertain for conventional underwriting, and collateral is minimal. Rather than proving bankability, founders make a case around market size, product differentiation, team strength and defensibility.

However, equity is rarely “free money.” The true economic cost is dilution of ownership and sometimes a shift in strategic priorities to maximize investor returns. Founders lose some strategic autonomy, and the company usually commits to faster growth trajectories, more aggressive hiring and larger marketing budgets. Hybrid instruments—revenue‑based financing, profit‑share agreements or convertible notes—try to rebalance this trade‑off. They allow investors to participate in upside while limiting fixed obligations, which can be especially attractive for service businesses with strong gross margins but uneven monthly revenue, like agencies or software firms transitioning from project work to recurring subscription models.

Data snapshot: what the numbers say about small business finance

Recent surveys across OECD economies indicate that access to finance remains one of the top three constraints cited by small and medium enterprises, coming in just behind finding skilled labor and managing input costs. In the U.S., Federal Reserve small business credit surveys show that roughly 40–50% of applicants for external financing receive the full amount requested, with smaller, younger firms facing higher denial rates. Online lenders have filled part of this gap, accounting for a rising share of loan originations, but often at significantly higher interest rates and shorter maturities than banks.

Globally, the value of outstanding SME loans has been growing modestly—typically in the low single digits annually in mature markets—while alternative lending (including crowdfunding, peer‑to‑peer platforms and revenue‑based finance) has been expanding at double‑digit rates from a smaller base. This indicates a structural shift rather than a simple post‑crisis rebound: traditional institutions retain volume dominance, yet flexible and data‑driven models are increasingly capturing growth segments, particularly in e‑commerce, SaaS and other digitally native industries where transaction‑level data provides more granular risk assessment than standard financial statements alone.

Forecasts: how financing options are likely to evolve

Looking ahead over the next five to ten years, analysts expect the small business finance ecosystem to become more fragmented but also more tailored. Open banking standards, real‑time accounting data and AI‑based credit scoring are likely to reduce information asymmetry between lenders and small firms. That should broaden access to many types of small business expansion loans, particularly for companies with short yet high‑quality digital track records—such as consistent online sales, low refund rates and strong customer retention metrics. At the same time, regulatory scrutiny on high‑APR products will probably intensify, nudging providers toward more transparent pricing.

On the equity side, micro‑VC funds, syndicate investing and revenue‑share vehicles are expected to keep growing, reflecting investors’ search for yield outside public markets and founders’ desire to avoid excessive dilution. Niche instruments that blend characteristics of debt and equity will become more common: for instance, loans with performance‑based interest rate step‑downs or warrants tied to specific growth milestones. Overall, the forecast is not that one “winner” financing model will dominate, but that matching capital type to business model, growth phase and risk tolerance will become more precise, aided by better data and more specialized intermediaries.

Economic aspects: cost of capital, risk and cash‑flow dynamics

From an economic standpoint, the choice between debt and equity hinges on three variables: cost of capital, risk distribution and cash‑flow timing. Debt usually has a lower explicit cost (interest rate) than equity’s implicit required return, but comes with rigid payment schedules and covenants. If growth investments underperform, debt can amplify downside risk by forcing distress sales or restructuring, especially when leverage ratios become too high. Equity, in contrast, absorbs volatility but demands a larger slice of long‑term profits, which can be more expensive if the business ultimately succeeds beyond expectations.

Another important dimension is how financing affects operating leverage. Using small business loans for growth to automate production, for example, increases fixed costs but may reduce variable costs per unit, raising sensitivity to revenue fluctuations. In strong markets, this improves margins and return on equity; in downturns, it can strain liquidity. Flexible credit lines and working capital instruments moderate this effect by linking financing more closely to sales cycles: as activity dips, utilisation naturally falls, limiting interest expense. This is why many experienced owners treat lines of credit as a buffer and term loans as strategic bets, each with a distinct role in the firm’s financial architecture.

Industry‑level impact: who gains and who risks falling behind

Access to tailored finance options doesn’t just change individual outcomes; it reshapes competitive dynamics within industries. Sectors with asset‑heavy models—manufacturing, logistics, construction—tend to benefit disproportionately from improvements in collateral‑based lending, as they can scale capacity faster once credit constraints ease. In contrast, creative and knowledge‑intensive industries rely more on equity and quasi‑equity, since their main asset is human capital. When investors become more comfortable underwriting intangible value, you often see an uptick in innovation, new entrants and faster product cycles.

Digital‑first platforms and data‑rich businesses are especially well positioned in this evolving landscape. Their ability to provide real‑time, verifiable performance metrics makes them attractive borrowers for fintech lenders, who can price risk dynamically. This, in turn, pressures traditional players that still rely on slower, paper‑based underwriting to adapt or lose market share. Over time, the spread in financing access becomes a structural advantage: firms that consistently secure the right kind of capital at the right price can invest more aggressively in technology, talent and customer acquisition, pulling away from competitors constrained to self‑fund or rely on expensive, short‑term credit.

Comparing approaches: how different options solve different problems

Rather than asking which are objectively the best financing options for small businesses, a more useful question is: “Which option matches the problem I’m trying to solve right now?” Growth challenges come in several flavors—temporary cash gaps, repeatable expansion, high‑uncertainty innovation—and each maps to a different financing logic. Trying to plug all of them with a single tool, like a general‑purpose loan or a business credit card, usually leads to suboptimal results, higher costs or unnecessary risk.

If your challenge is bridging timing differences—payroll and supplier invoices due before customer cash comes in—flexible lines of credit and working capital instruments are usually more appropriate than long‑term debt or equity. When you’re rolling out a proven business model to new locations or markets, structured small business expansion loans and equipment financing typically make more sense, since you can model payback with some confidence. For fundamentally new products or markets where outcomes are highly uncertain, equity or revenue‑based financing is often safer than leveraging the balance sheet heavily, because it doesn’t force fixed repayments during the riskiest phase.

Practical decision framework: narrowing your choices

You can simplify the comparison by running your situation through a few key questions:

1. How predictable are future cash flows from this growth initiative?

The more predictable and contract‑based your revenue (for example, subscriptions or long‑term contracts), the more comfortable you can be with term loans. Highly volatile or experimental revenue streams argue for equity or performance‑linked repayment structures instead of rigid amortization.

2. Is the spending one‑off or recurring?

One‑off, asset‑creating expenditures—like buying machinery or refurbishing a new storefront—fit long‑term debt. Recurring, variable costs—marketing campaigns, inventory replenishment—align better with small business lines of credit for growth or other revolving facilities that can expand and contract with your needs rather than locking you into a fixed balance.

3. What is your tolerance for dilution versus default risk?

If you value retaining full control and are confident in near‑term profitability, you might lean toward loans even if they feel conservative. If you prioritize downside protection and are willing to share upside, equity and hybrids can be healthier, especially in turbulent markets where cash‑flow surprises are common.

4. How fast do you actually need the money?

Bank loans and government‑backed schemes often have lower rates but longer approval times and stricter documentation. Online lenders, factors and some alternative providers can fund within days, but at a premium cost. Matching urgency to price avoids overpaying for convenience when a slower, cheaper option would suffice.

5. What will this financing look like on your balance sheet in 3–5 years?

Project your leverage, cash coverage ratios and ownership structure forward. An option that looks harmless now can constrain you later—for example, stacking short‑term advances that become a permanent burden, or giving away a large equity stake early that makes later rounds complicated or dilutive for you and your team.

Bringing it together: a portfolio mindset to financing growth

The most resilient small businesses rarely rely on a single funding source. Instead, they assemble a financing “portfolio”: a mix of term loans for long‑lived assets, revolving credit for working capital, and, when appropriate, equity or quasi‑equity for riskier bets. This diversified approach recognizes that growth is not a uniform project but a sequence of experiments, replications and optimizations, each with its own risk and cash‑flow profile. By consciously matching instruments to these profiles, owners can grow faster without losing sleep over every economic wobble or industry shock.

In the end, choosing among small business loans for growth, equity injections and alternative structures is less about chasing the lowest headline rate and more about aligning incentives, timelines and risk. When the financing structure reinforces how your business actually operates—seasonality, margin structure, customer behavior—you free up mental bandwidth to focus on strategy and execution. As data‑driven underwriting, fintech platforms and new investor models continue to mature, the businesses that understand these trade‑offs will be best positioned not just to survive, but to compound their advantages over time.