Why talking about money with kids in 2025 is completely different

If you learned about money through pocket cash and a piggy bank, your child lives in another universe. By age 8–9 many kids in 2025 have already paid for something with a phone, watched parents tap a smartwatch at the supermarket, and seen a YouTuber say “link in description” to promote a financial app. Physical money is disappearing from their daily life, but their access to digital spending is growing. That’s why financial education for kids can’t be an optional “someday” topic anymore — it has to go hand in hand with how they already use technology every day.

We no longer teach kids only how to count coins. We help them understand what happens when they click “subscribe,” agree to in‑app purchases, or connect a card to a gaming account. If adults still think of money as a stack of bills in a wallet, children see it as numbers on a screen that go up and down with a swipe. The good news: this makes abstract financial concepts easier to visualize. The bad news: one impulsive tap can cost 20 dollars in seconds. Your role is to build habits and thinking patterns that will stay with them when they eventually control their own bank account, not just their game skins.

—

Age-by-age roadmap: what to teach and when

3–6 years: From “shiny coins” to basic choices

At this age, kids can’t yet grasp interest rates or budgeting apps, but they clearly understand choice: “If I buy this, I can’t buy that.” Start with concrete, visible tools. Give them three jars or boxes: “Spend”, “Save”, “Share”. When they receive money — from you, relatives, or small rewards — let them physically divide it between the jars. Even if actual payments in your family are mostly digital, these tangible steps anchor the idea that money is limited and must be directed somewhere on purpose.

Real‑life example: a parent in Berlin shared that his 5‑year‑old was obsessed with a cartoon toy worth around €15. They agreed the child would get €2 every week. Each Sunday the kid placed the coins into the “Save” jar and colored a small square on a paper “goal tracker”. After eight weeks, they counted the saved amount, paid together at the store, and the child proudly carried the receipt home. That single experience often does more than dozens of lectures about “saving is good.”

Technical note – what kids understand at 3–6:

At this stage children operate in a very concrete way: they understand “more” and “less,” but not future value or delayed interest. So aiming for 3–4 simple concepts is enough: money doesn’t appear by magic; it can be used only once; you can wait for something; and you can give some of your money to others.

—

7–10 years: Introduce digital money, not only piggy banks

By 8 or 9, children can follow simple rules and start seeing patterns. This is the perfect moment to bridge the gap between coins and the invisible world of cards and apps. If you use contactless payments, show them the transaction in your banking app. Let them compare: “We had $530 before the supermarket, now we have $487. That bag of groceries was $43.” Connecting shopping trips with numbers on a screen makes “tapping” feel real, not like a video game.

Many parents start a simple “family money management for children course” each month. It’s nothing formal: just 20–30 minutes on a Sunday, where you discuss one short topic — what a budget is, how subscriptions work, why some ads push you to buy. The key is repetition and real examples, not one serious conversation twice a year. In 2024 and 2025, surveys in North America and Europe show that children in this age range increasingly ask about online games and subscriptions, not toys. That’s your signal to focus on recurring payments, not only one‑time purchases.

—

11–14 years: Pocket money becomes a mini budget

Preteens are ready for more responsibility. Here, money is no longer only a teaching prop but a real tool. Instead of giving random amounts when they ask, switch to a regular allowance with clear expectations. For example, a 12‑year‑old might receive $40–$60 per month and be responsible for small treats, inexpensive gifts for friends, and part of their entertainment spending. The idea is that when the money is gone, it’s gone — no “emergency top‑ups” for impulse buys.

This is the stage when online financial literacy programs for kids are especially helpful. Many banks and fintech companies now offer youth accounts and apps with parental controls, spending limits, and built‑in lessons. In 2025, some of these apps can automatically categorize spending (games, snacks, transport) and show a weekly “report” with simple infographics. Sit down once a month and review that together the way a manager reviews a project. Ask: “What surprised you? What could you change next month?” Let them draw conclusions instead of lecturing them.

Technical note – a simple allowance rule of thumb:

A common guideline is weekly allowance ≈ child’s age in dollars (or local equivalent). For a 12‑year‑old, that’s about $12 per week. This is not a law; adjust for your finances and local prices. What matters more is consistency: the same day each week, no random bonuses, and clear rules on what this money covers.

—

Core money lessons every young learner needs in 2025

Lesson 1: Money is limited, attention is not

In a world of infinite streams, videos, and games, the only thing clearly finite is money. But kids often feel the opposite: games are unlimited, so in‑game purchases also seem infinite. Explain that companies design systems to keep them clicking: limited offers, countdown timers, loot boxes. Show them one example in a game they love and break it down: “See this special chest? It costs $3 and appears for 24 hours. The goal is to make you feel like you’ll miss out if you don’t pay now.” You’re not demonizing games, you’re training them to recognize nudges.

A practical daily rule: before any non‑planned purchase, ask your child to pause for 24 hours. When they want a new skin or accessory, say “If you still want it tomorrow at this time, we’ll talk again.” Many 9–13‑year‑olds forget about that purchase within a day. You’ve just given them a micro‑lesson in impulse control.

—

Lesson 2: Save with a purpose, not in the abstract

Telling a child “saving is important” means almost nothing if they don’t have a clear goal. Help them design one short‑term and one medium‑term target. A short‑term goal might be a $20 accessory or a board game for the next school break. A medium‑term goal might be $100 for a big toy, a concert ticket, or part of a gadget they really want. Clearly define the amount, the deadline, and how much they need to set aside each week to get there.

You can reinforce this with simple digital tools. Some youth‑focused banking apps now let kids create separate “pots” for goals with a progress bar. Combine that with physical visuals: a printed “thermometer” on the fridge they color in every time they add money. Kids in real families often respond more strongly to seeing progress than to the actual amount. When the bar is at 80%, they become more motivated to say no to small temptations to reach the finish line.

Technical note – basic interest in kid language:

If your child has $50 and a kids’ savings account gives 2% per year, that’s $1 in a year. Don’t focus on the 2%; talk about the $1: “The bank thanks you for keeping money there and adds a bit. The more and longer you keep, the more ‘thank‑yous’ you get.” For most children under 13, concrete extra dollars matter more than percentage formulas.

—

Lesson 3: Income has many sources (but not all are equal)

The 2020s changed what kids see as “work.” Many no longer dream only of being doctors or teachers; they see streamers, designers, coders, NFT artists, or YouTube creators. Your job is not to crush those dreams but to anchor them in financial reality. Differentiate between:

– Guaranteed income: salary, fixed payments for chores or part‑time jobs.

– Variable income: sales of crafts, tutoring, odd jobs for neighbors.

– Speculative or “maybe” income: trying to go viral, get donations, or flip digital items.

Use examples around you. If a teen wants to start a small Etsy store or sell digital art, help them build a basic cost‑revenue picture: “You spend $30 on materials or tools, aim to sell for $60, after platform fees and taxes you might keep around $45. Is it worth your time?” This beats vague talk about “entrepreneurship” and gives them a taste of how real‑world projects are evaluated.

—

Modern tools that actually help (instead of just distracting)

Digital apps and courses: turning screens into allies

Today, you can’t realistically keep kids away from screens, so the question becomes: which tools guide them and which trap them? Well‑designed online financial literacy programs for kids focus on bite‑sized modules: 5–10 minute lessons, mini quizzes, and interactive scenarios (“You received $30 birthday money; what do you do?”). Many parents run through these together with their children once a week. This collaboration turns learning into a joint project instead of a test.

If you want more structure, look for platforms that resemble a money management for children course, not just a one‑off game. Signs of quality include clear age ranges, transparent curriculum (earn, spend, save, donate, protect), and parental dashboards to track progress. Avoid anything that links learning to promoting specific cards or loans too aggressively — in 2025 the line between education and marketing can be thin, so read the fine print before connecting accounts.

—

Games to teach children about money that don’t feel boring

Kids learn remarkably well through play, especially when it feels like a challenge rather than a lecture. Alongside classic board games about buying, renting, and trading, there are modern games to teach children about money that reflect digital realities: managing a virtual café, building a city with a budget, or running a small online shop. The aim is not perfect realism but exposing them to trade‑offs: you can’t improve everything at once, so what do you prioritize?

You can also design simple “family economy” games at home. For example, set a monthly “family project budget” of $30. Ask the children to propose how to use it: a movie night, baking supplies, materials for a craft, or a short trip. Let them pitch ideas, then vote and track actual spending against the initial plan. This not only teaches math but also negotiation, compromise, and that budgets are about choices, not restrictions.

—

Story time: what works in real families

Case 1: The 9‑year‑old gamer and accidental overspending

A family in Toronto discovered that their 9‑year‑old had spent around $120 on in‑game items over two months. The purchases were technically allowed because the game was connected to a parent’s card and used face recognition instead of a password. Rather than banning games altogether, the parents sat down and printed the monthly statement. Together they highlighted each game transaction in a different color, then put the total on a sticky note: “This equals three family cinema trips or one month of sports lessons.”

They created a new rule: all digital purchases had to come from the child’s own allowance, plus the card was removed from the console. The boy started asking, “How many weeks of saving is this skin?” Within a few weeks, he cut his spending by more than half. The emotional shock of seeing the total and the concrete comparison with other joys he understood made the impact, not parental anger.

—

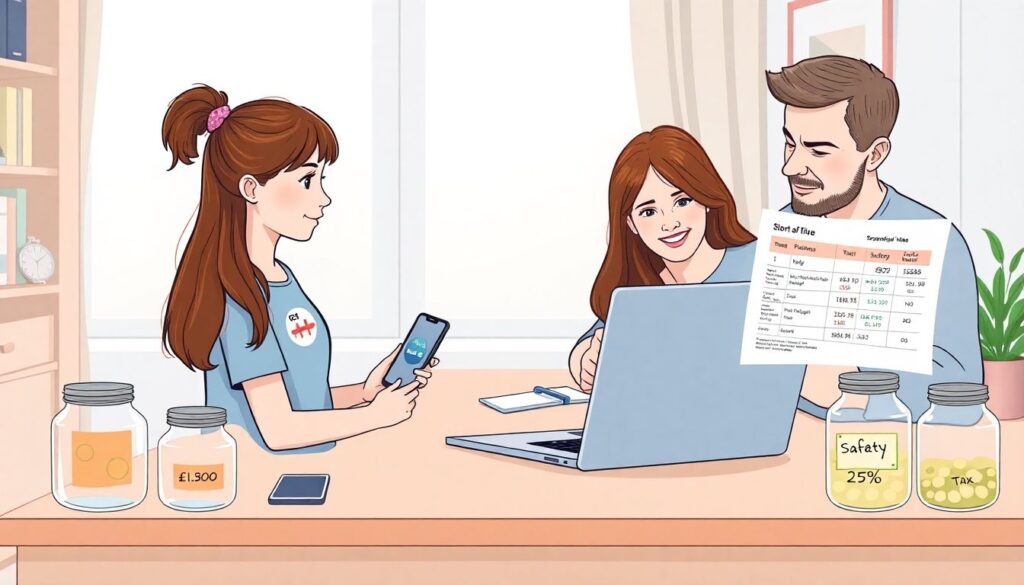

Case 2: Teen content creator meets taxes and reality

A 14‑year‑old girl in the UK began earning money from short‑form videos — small sponsorships and platform bonuses. In one year she made about £1,300. Her parents used this as a structured learning project. Together they tracked income in a spreadsheet, set aside 25% in a separate “tax and safety” pot, 25% for savings, 25% for reinvestment (equipment, better microphone, lighting), and 25% for free use. They also had a call with a tax advisor through a youth entrepreneurship program so she could hear, from a professional, that earnings from content are still taxable.

This experience taught her three big lessons: income can be irregular, governments expect a share, and smart creators treat their activity like a small business, not like magic money from the internet. By 16, she already had two years of mini business management under her belt — a huge head start compared to many adults.

Technical note – introducing taxes without fear:

Explain taxes not as punishment, but as membership fees for living in a functioning society: roads, schools, hospitals. Use concrete ratios: “If you earn $100 from your project, imagine $20–$30 goes to taxes and social fees. Better to plan for that from the start than be surprised later.”

—

Books and stories that make money talk feel natural

Using books instead of lectures

Many parents struggle to find the right words, especially if their own relationship with money is complicated. This is where stories help. The best books to teach kids about money don’t just say “save money”; they show relatable characters dealing with allowance, peer pressure, or wanting the latest gadget. For younger kids, picture books with simple plots about sharing, waiting, and making choices work best. For older ones, short novels or graphic stories about starting a mini business or solving a financial problem are effective.

Try reading one money‑related book per year, adjusting for age. Don’t turn it into a heavy “lesson.” Read together, then ask open questions: “What would you do in this situation?” or “Why do you think the character felt bad after buying that?” When children see money decisions in stories, it becomes easier for them to talk about their own mistakes and worries without feeling judged.

—

Hot topics of 2025 you shouldn’t ignore

Digital wallets, BNPL, and invisible debt

In many countries, teens over 13 can now sign up for digital wallets or prepaid cards connected to Apple Pay, Google Pay, or local equivalents — often with minimal friction. At the same time, “buy now, pay later” (BNPL) options have spread from adults into youth‑oriented platforms, including online fashion and tech stores frequently visited by older teens. They may be only a couple of clicks away from committing to future payments they don’t fully understand.

Teach a simple rule of thumb: if you can’t see clearly how you will pay for something from your next regular income, you shouldn’t promise the money. Draw it: “Today: 0, Next month: –$25, Month after: –$25.” Show how small recurring payments stack. A streaming service here, a gaming pass there, a “cheap” BNPL purchase — suddenly a teen’s entire allowance for the month is already allocated before it even arrives.

—

Crypto, meme stocks, and the “get rich yesterday” culture

By 2025, even 11–12‑year‑olds have heard of Bitcoin, meme coins, and people “getting rich” on short‑term trading. You don’t need to turn them into experts in blockchain, but you do need to inoculate them against hype. Emphasize that any asset whose price can go up very fast can also fall very fast. Show a year‑long price chart of a well‑known cryptocurrency: let them see the peaks and drops. Numbers speak louder than warnings.

Teach them the difference between investing and speculating using everyday examples. Investing is like planting a tree for shade in a few years — boring, slow, but reliable when diversified. Speculating is like betting whether it will rain tomorrow. Sometimes you’re right, sometimes not, but it’s not a plan. If they show interest, guide them first towards learning about diversified funds and long‑term horizons rather than individual coins or meme stocks promoted by influencers.

—

Your action plan: how to start this month

To make all of this concrete, pick two or three simple steps you can implement within the next four weeks. It doesn’t have to be perfect; consistency matters more than strategy brilliance. You might choose:

– Introduce or formalize a regular allowance with clear rules on what it covers.

– Set up three jars or digital “pots” for Spend / Save / Share with a specific goal for each.

– Schedule one weekly “money talk” of 15–20 minutes using a book, app, or family budget example.

Over time, add layers: a basic budget at 11–12, a first savings account, a conversation about taxes and online safety, a look at how ads and influencers are funded. Think of it as a long‑term project where your child becomes the “chief financial officer” of their own small life.

In a world where they can spend money with a tap before they fully understand what a contract is, early and honest financial education for kids is one of the most protective gifts you can offer. If you weave money lessons into everyday life — shopping, gaming, holidays, even family disagreements — your child will grow up seeing money not as a source of stress or magic luck, but as a tool they can understand and manage thoughtfully. That mindset will be worth far more, in the long run, than any single allowance or birthday gift.