Understanding the Real Cost of Investing

What Investment Fees Actually Are

When you start investing, the list of charges can feel like alphabet soup: TER, MER, load, spread, custody, advisory. Instead of memorising every term, focus on one idea: every fee takes a slice of your returns, year after year. In practice, fees show up in three places: when you buy or sell (trading and brokerage costs), while you hold the investment (fund and platform fees), and when you get advice (planner or robo‑advisor charges). Think of this section as *investment fees explained for beginners*: your job is not to pay zero, but to understand exactly what you’re buying for every dollar of fees and whether the benefit is truly worth the drag on long‑term growth.

Why Beginners Should Care About Small Percentages

A 1% fee sounds innocent until you do the math. Suppose two people invest with identical returns before fees, but one pays 0.2% a year and the other 1.5%. Over 30 years, the higher‑fee investor can easily end up with tens of thousands less, purely because of that gap. Fees compound in reverse: instead of growing your money, they grow the distance between you and your goals. That is why people hunt for *low cost index funds with lowest fees* and obsess over expense ratios. You don’t need to become a fee maniac, but you do need a system for checking charges regularly, just like you’d check recurring subscriptions on your bank statement.

Tools You Need to Analyse Your Fees

Essential Documents and Reports

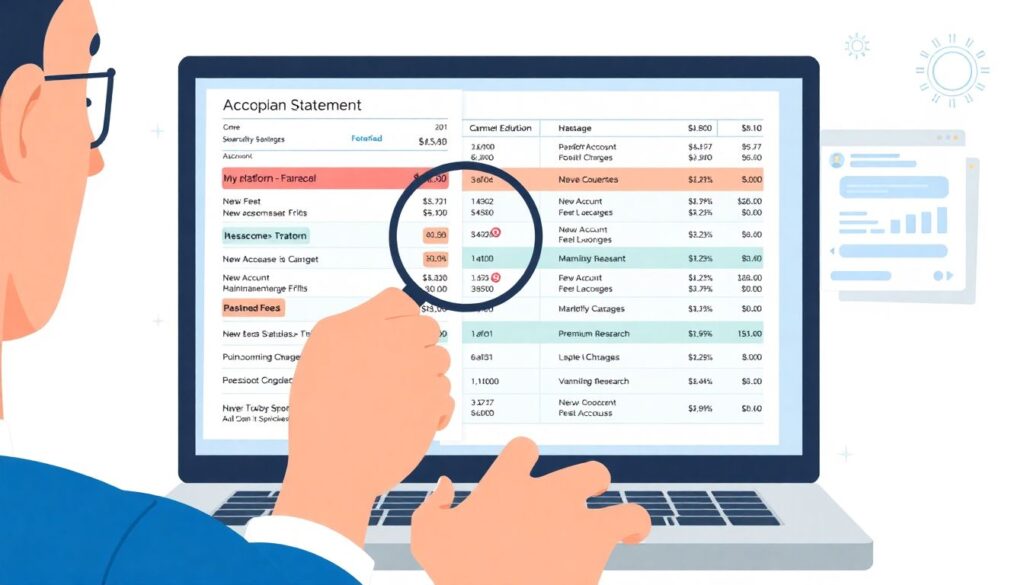

Before you can optimise anything, you need raw data. The basic “toolkit” is surprisingly simple: your brokerage statements, fund fact sheets, and fee disclosure documents from platforms and advisors. These show trading commissions, account maintenance fees, and ongoing fund expenses. Beginners often skip the small print, yet that’s where the real cost is buried. To *compare brokerage fees for beginners*, line up a few recent statements from different providers, note how many trades you made, the size of each trade, and what you paid. It’s a bit like reading a phone bill: once you know which line items drive the total, you can start cutting the right ones without overreacting.

Digital Tools and Online Calculators

Paper is a start, but digital tools make the analysis less painful. Many of the *best low fee investment platforms* now include fee dashboards that estimate how much you pay annually and how that might affect your future balance. You can also use independent online calculators: plug in your portfolio size, expected returns, and current expense ratios, then test how lower fees would change the outcome. Spreadsheet lovers may build a simple model that tracks each holding, its cost, and its fee level. The goal is not perfection; it’s to get a realistic, quantified view of the price you’re currently paying for convenience, advice, or active management, so you can judge whether those services deserve their slice.

Step‑by‑Step: Auditing and Cutting Your Fees

Practical Process for Beginners

1. Start by listing every account you have: brokerages, retirement plans, robo‑advisors, and any managed portfolios. Note balances and main holdings.

2. For each account, identify headline fees: trading commissions, platform charges, and each fund’s expense ratio. Ignore jargon; you just need percentages and flat dollar amounts.

3. Rank holdings by cost. High‑fee active funds and structured products usually float to the top, while broad index trackers sit near the bottom.

4. Decide what you’re willing to swap. Could a pricey active fund be replaced by a cheaper ETF with similar exposure? This is the core of *how to reduce investment management fees* without wrecking your asset allocation.

5. Implement changes gradually, considering taxes, bid‑ask spreads, and any exit penalties so the cure doesn’t cost more than the disease.

Comparing Different Approaches to Lowering Fees

DIY with Broad Index Funds

One popular route is to go mostly DIY and build a simple portfolio around broad market trackers. You buy a few diversified ETFs or mutual funds that mirror the global stock and bond markets, then hold them for years. This approach leans heavily on *low cost index funds with lowest fees*, often undercutting both active funds and robo‑advisors. The upside is clear: minimal ongoing costs and full control. The downside is behavioural risk. You must rebalance yourself, resist market timing, and stay disciplined during volatility. For people who enjoy a bit of number‑crunching and can stick to a plan, DIY indexing tends to deliver excellent fee‑adjusted results over the long haul.

Robo‑Advisors and Bundled Solutions

Robo‑advisors promise automation: you answer a questionnaire, they build and maintain a diversified portfolio, often with tax‑loss harvesting and rebalancing baked in. Their all‑in fees are usually lower than traditional advisors but higher than a pure DIY index setup. When you *compare brokerage fees for beginners* across robos and old‑school brokers, you’ll see that robos charge a percentage of assets plus underlying fund costs, while many brokers earn mainly from trading and fund commissions. Robos suit investors who want a low‑effort, rules‑based system and are comfortable delegating. The trade‑off is paying extra every year for convenience you might, with some discipline, partially replicate on your own.

Human Advisors and Hybrid Models

Traditional advisors often come with the highest headline percentages, but the story is more nuanced. A good planner combines investment management with tax planning, estate guidance, and behavioural coaching—things a robo can’t fully replicate yet. Hybrid models, where you get a human plus a robo platform, sit in the middle on both price and service. Your task is to look past labels and examine value: if an advisor charges 1% but helps you avoid costly mistakes, the fee may be justified; if they simply pick expensive funds and rarely call, it’s dead weight. When you see *investment fees explained for beginners*, remember that “expensive” can be acceptable if the benefit is clear, measurable, and aligned with your goals.

Troubleshooting Common Fee Problems

Spotting Hidden and Unexpected Costs

Even after a clean‑up, odd charges can creep in. Sudden rises in platform fees, new account maintenance charges, or “premium research” add‑ons can quietly inflate your costs. Treat any unexplained line item as a bug to debug. Look up each fee in your provider’s schedule and ask support to clarify anything vague. Sometimes a supposedly “free” account becomes costly if you trade frequently or fall below a minimum balance. In such cases, it may be time to *compare brokerage fees for beginners* again and check if another provider offers a structure that better matches how you actually invest, not how their marketing suggests you will.

When Switching Platforms Backfires

Moving to a cheaper platform or fund is not automatically a win. Transferring accounts can trigger exit fees, tax events, or time out of the market. If you chase every new low‑cost offer, transaction costs and spread slippage can offset the savings. Before switching, calculate how long it will take for lower ongoing fees to compensate for one‑off costs. This is where analytical patience beats impulsive action. Sometimes it’s wiser to keep an old account open but redirect new contributions to one of the *best low fee investment platforms*, gradually shifting your overall cost downward without sudden disruption. Lower fees are a goal, but stability and a coherent plan still matter more.