Rethinking the “Magic Number”: Why One Size Never Fits All

Most people hear about a so‑called “magic retirement number” and assume there’s a universal target – 1 million, 2 million, or some other big round figure. In reality, the question isn’t just “how much money do I need to retire?” but “what cash flow, risk level and flexibility do I personally need to stay calm and solvent for 30–40 years?” Вenefits, tax regimes, healthcare costs, expected longevity and even your appetite for uncertainty make that number radically different from one person to another, so a rigid benchmark often creates more anxiety than clarity.

Core Formula: From Pile of Money to Stream of Income

Before talking forecasts or market risks, it helps to translate your lifestyle into annual spending and then into a capital requirement. The classical approach is to start from desired annual expenses in retirement, subtract predictable income (pensions, annuities, rental cash flow), and then use a withdrawal rate to estimate how large a portfolio you need. This transforms the abstract concept of a “magic number” into a concrete asset-liability matching problem, rather than a guessing game based on headlines.

The 4% Rule – and Why It’s Only a Baseline

In financial planning the “4% rule” is widely cited: in theory you can withdraw 4% of your initial portfolio per year (inflation-adjusted) and have a high probability of not running out of money over 30 years. That implies a simple inverse relationship: desired income × 25 ≈ target portfolio. If you want $60,000 per year from investments, a rough target is $1.5 million. This is a starting point, not a law of nature, especially in a world of higher volatility and uncertain bond yields.

Dynamic Withdrawals: A Non‑Standard, More Realistic Approach

Static rules ignore the fact that retirees can and do adjust spending. A more robust strategy uses dynamic withdrawal policies that respond to markets and portfolio performance. For instance, you can increase withdrawals after strong market years and tighten the belt slightly after drawdowns. Technically это похоже больше на управление рисками денежных потоков (cash‑flow risk management), чем на жёсткую формулу, и позволяет повысить устойчивость портфеля без драматического увеличения стартового капитала.

Statistics: Where People Actually Stand vs. Where They Need to Be

Empirical data shows that median retirement balances are often far below what actuarial models suggest is adequate. Surveys in the U.S. regularly show that people in their 50s frequently have retirement accounts under $200,000, while planning tools suggest several times that level is needed for a typical middle‑class lifestyle. When people search something like “how much money do I need to retire calculator”, they usually discover a gap between current savings and target capital that looks intimidating but can be addressed with better structure and timing.

“Retirement Savings by Age”: Why Rules of Thumb Mislead

Popular rules such as “by age 30, have one year of salary; by 40, three times; by 50, six times” are oversimplified proxies. When you see charts about retirement savings by age how much should i have, they rarely account for late‑career income spikes, varying pension coverage, career breaks, or entrepreneurship. Two people with identical ages and salaries can have very different risk capacities and asset bases – for example, a doctor with a defined benefit plan and a freelancer relying solely on an investment portfolio face distinct constraints.

Non‑Linear Savings Trajectories

In practice, wealth accumulation is rarely linear. Early years often combine student debt, low earnings and high housing costs; the real compounding effect kicks in later, when income rises and contribution rates can increase. This means a 30‑year‑old behind the textbook target isn’t doomed. What matters is the savings rate relative to disposable income over the next 10–20 years, asset allocation efficiency, and how long you plan to work. Важно сместить фокус с «я отстаю» на «как оптимизировать траекторию накоплений и рисков».

Forecasts: Longevity, Markets and Policy Risk

Retirement today isn’t a 10–15‑year event; for many it’s a 30–40‑year financial project. Longevity projections keep stretching, especially in developed economies, and that lengthens the liability side of the balance sheet. Meanwhile real yields, equity risk premiums and tax rules do not remain static. The “magic number” therefore is conditional on forward‑looking assumptions: expected real returns, inflation, healthcare inflation differentials and the probability of policy changes affecting social benefits or tax treatment.

Longevity and Sequence‑of‑Returns Risk

Two technical risks drive much of the uncertainty. Longevity risk is the chance you outlive your assets; sequence‑of‑returns risk is the danger of poor market performance early in retirement, when withdrawals magnify losses. Even if average returns match forecasts, bad timing in the first 5–10 years can permanently impair the portfolio. That’s why a retiree in 2035 may need a higher or lower “magic number” than someone retiring today, depending on when market cycles and interest‑rate regimes shift.

Macroeconomic Scenarios: Inflation and Real Yields

Economic forecasts increasingly consider regimes rather than single-point estimates. A low‑inflation, low‑rate environment favors growth assets but leaves conservative savers exposed to shortfall risk. By contrast, high inflation and higher nominal yields can erode fixed income in real terms while supporting some real assets like property or commodities. Ваш «магический номер» чувствителен к этим сценариям: при низких реальных ставках портфель должен быть крупнее, а при более высоких ставках – структура может смещаться в сторону облигаций и аннуитетов.

Economic Aspects: What the “Magic Number” Really Depends On

The capital required to retire comfortably is not purely a function of lifestyle; it also reflects productivity growth, wage dynamics, taxation, and healthcare systems. When productivity and wages grow faster than inflation, future retirees can potentially save more in the final decade of work. Conversely, if real wage growth stagnates, households rely more heavily on investment returns and must either increase savings rates or accept a lower consumption level in retirement.

Tax Systems and Replacement Rates

Your gross “magic number” is influenced by the net replacement rate you aim for – the percentage of your pre‑retirement income you want to maintain. Tax brackets and deductions in retirement differ from those in your working years. For some, the effective tax rate drops, allowing the same lifestyle from lower gross income. Others, especially high earners with tax‑deferred accounts, may see large required minimum distributions pushing them into higher brackets. Наряду с этим, различия между странами по пенсионным выплатам и медицинской страховке радикально меняют требуемый объём частных накоплений.

Housing, Debt and Non‑Financial Assets

Housing status drastically alters the capital needed. Owning a home outright reduces required cash flow but concentrates risk in a single illiquid asset. Conversely, renting provides flexibility but demands higher liquid assets to cover lifetime housing costs. Non‑financial assets such as private businesses, royalties or intellectual property can serve as alternative income streams, but they carry idiosyncratic risk and often require active management, особенно на ранних этапах «выхода на пенсию» при частичной занятости или консультировании.

Breaking Down the “Magic Number” for Different Retirement Ages

The earlier you retire, the longer your portfolio must last, and the more important growth assets become. When people ask “how much do I need to retire at 55”, the answer is almost always “more than if you stop at 67”, not only because you need to fund extra years, but also because you may not yet qualify for full public benefits or subsidized healthcare. This stretches the funding gap and increases exposure to market and policy changes over a longer horizon.

Early Retirement (FIRE and Semi‑Retirement)

The Financial Independence, Retire Early (FIRE) movement pushed withdrawal rates as low as 3–3.5% for ultra‑long horizons. However many “retirees” in this community practice semi‑retirement, monetizing hobbies, freelancing or building location‑independent businesses. This creates a hybrid structure: capital covers a base level of expenses, while variable income provides a buffer. Технически это ближе к управлению человеческим капиталом, чем к классической фиксированной пенсии, и позволяет снизить стартовый «магический» капитал без существенного роста рисков.

Standard Retirement Ages and Flexible Phasing

For those aiming at traditional retirement ages (60–67), a phased approach – reducing hours, changing roles, consulting – can be more powerful than squeezing every last dollar into savings. By working even 2–3 extra years part‑time, you compress the decumulation period, maintain human capital and defer drawing down investments, effectively reducing the necessary portfolio size. This kind of labor‑market flexibility is an underrated lever compared to narrow focus on accumulated assets.

Behavioral Pitfalls: Why Many Miss Their Target

Even with accurate models, human behavior often derails financial plans. Under‑saving, poor diversification, market timing based on emotion and lifestyle inflation in peak earning years can all shift the magic number out of reach. Behavioral finance highlights loss aversion and myopia: people hate realizing losses and over‑weight short‑term market noise, leading to suboptimal asset allocation and panic selling during downturns when long‑term discipline is most crucial.

Anchoring to Arbitrary Numbers

One subtle issue is anchoring: if everyone talks about needing $1 million, your brain fixates on that figure regardless of your actual situation. For a frugal person in a low‑cost region with strong public benefits, that number may be overly conservative; for a high‑spending household in an expensive city, it may be grossly insufficient. Отказ от «магических» якорей в пользу индивидуального моделирования денежных потоков помогает принимать более рациональные инвестиционные и карьерные решения.

Over‑Conservatism vs. Over‑Optimism

Being too cautious (holding excessive cash, avoiding equities) can be as damaging as excessive risk‑taking, because you expose yourself to inflation and longevity risk. Conversely, assuming double‑digit returns or ignoring healthcare inflation is a recipe for disappointment. The art lies in aligning portfolio risk with both your psychological comfort and your objective time horizon, using scenario analysis rather than single‑point estimates.

Non‑Standard Solutions: Beyond “Save More, Spend Less”

Instead of relying solely on a larger investment account, you can engineer retirement security using multiple levers. Combining financial engineering with lifestyle design and labor flexibility produces a more resilient plan than simply pushing for the biggest possible portfolio. Here are some unconventional, but technically sound, approaches to compress your required “magic number” without sacrificing quality of life.

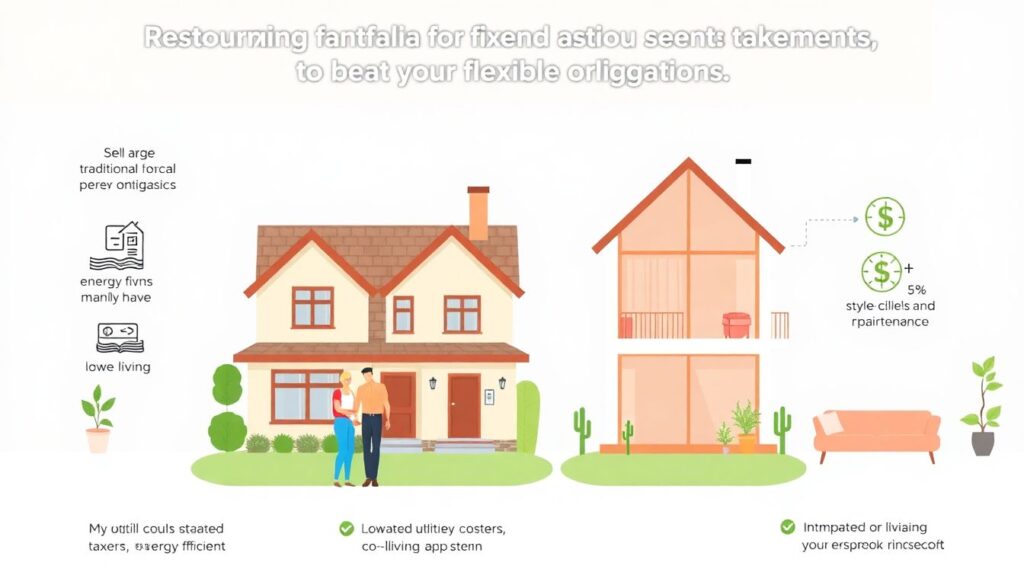

1. Turn Fixed Costs into Variable Ones

By restructuring fixed obligations into more flexible arrangements, you reduce the baseline income your portfolio must cover. For instance, selling a large home and moving to a smaller, more energy‑efficient property or a co‑living arrangement can lower utility, taxation and maintenance costs. В результате ваши обязательства становятся ближе к переменным расходам, зависящим от стиля жизни, а не от жёстко заданных платежей, что облегчает адаптацию бюджета при рыночных просадках.

Practical Levers

– Downsizing property, relocating to regions with lower taxes and living costs

– Substituting ownership (cars, vacation homes) with on‑demand access (car‑sharing, rentals)

– Negotiating long‑term service contracts (internet, insurance) for lower rates and predictability

2. Build “Micro‑Pensions” from Multiple Income Streams

Instead of relying entirely on one large portfolio, think in terms of micro‑pensions: small, diversified income streams that layer together. Examples include royalties from digital products, modest rental income from a studio or co‑owned property, part‑time teaching, or recurring revenue from software tools. Technically, this spreads idiosyncratic risk and reduces the withdrawal burden on your main investment portfolio, shrinking the level of capital it must supply.

Examples of Micro‑Pensions

– Niche online courses or subscription communities generating modest but steady cash flow

– Co‑investing in small rental units with partners instead of a single large property

– Licensing creative works or software on a recurring basis rather than one‑off sales

3. Geography and “Arbitrage” of Costs

Geo‑arbitrage – relocating to areas with lower cost of living while keeping some income denominated in stronger currencies – can drastically lower the required “magic number.” A portfolio barely sufficient in an expensive metropolis might provide a high standard of living in a mid‑cost country with adequate healthcare infrastructure. Это не только эмиграция: иногда достаточно переезда в менее дорогой регион внутри одной страны, чтобы снизить долговую нагрузку и увеличить ставку сбережений ещё до выхода на пенсию.

Technology, Tools and the Rise of Personalized Planning

The explosion of digital planning tools has changed how individuals calculate their targets. Rather than a single static estimate, modern software runs Monte Carlo simulations, scenario analysis and tax‑aware optimization to show probabilities of success. When someone types “what is the magic retirement number to retire comfortably” into a search engine today, they can be directed to interactive platforms that integrate spending patterns, expected pensions and portfolio composition into a dynamic projection rather than a flat answer.

Algorithms, Advisors and Hybrid Models

Robo‑advisors use algorithms to automate asset allocation and rebalancing, often at low cost, while human advisors specialize in complex cases: business owners, cross‑border taxation, estate planning. For many, a hybrid model – automated investment management plus strategic guidance – offers the best balance of cost and nuance. When you look for the best retirement planning services near me, what you are really searching for is this combination of behavioral coaching, tax optimization and data‑driven portfolio design.

Data‑Driven Customization

Improved access to financial data enables advisors and individuals to benchmark actual progress against customized glide paths rather than generic age‑based rules. В процессе планирования можно моделировать различные сценарии: частичная занятость, переезд, изменение семейного состава, запуск бизнеса. Эти модели превращают пенсию из точки в будущем в управляемый, адаптивный проект, где «магический номер» пересматривается и калибруется по мере изменения исходных данных.

Impact on the Financial Industry and Broader Economy

As populations age and defined benefit pensions give way to defined contribution plans, responsibility for retirement security shifts from institutions to individuals. This reshapes capital markets and the structure of the asset‑management industry. Demand increases for low‑cost index funds, liability‑driven investment strategies and products that convert capital into predictable cash flows, such as annuities and longevity insurance, though these instruments also raise concerns about complexity and transparency.

Industry Response: Product Innovation and Regulation

Asset managers and insurers are building products tailored to decumulation rather than accumulation, integrating guaranteed income features, downside protection and tax optimization. Regulators respond by tightening disclosure standards and fee transparency, particularly for complex annuities and structured products. The interplay between consumer demand for security and regulatory pressure for simplicity is already altering product design, fee structures and distribution channels across the industry.

Macro‑Level Consequences

At a macroeconomic level, higher aggregate savings for retirement affect capital formation, interest rates and even labor participation among older individuals. If large cohorts delay retirement due to inadequate savings, labor markets may see increased competition in certain sectors and slower turnover, while governments face pressure to reform public pension systems. Одновременно растущие пенсионные активы усиливают роль институциональных инвесторов на рынках, влияя на волатильность, корпоративное управление и доступность капитала для бизнеса.

Putting It All Together: Your Personal “Magic Number”

In the end, the “magic number” is less a single figure and more a living model built around your cash‑flow needs, risk tolerance, human capital and lifestyle design. Instead of obsessing over whether you’ve hit a universal benchmark, construct a flexible framework: estimate realistic spending, map out income sources, stress‑test different return scenarios, and revisit assumptions regularly. Rather than treating retirement as a cliff, view it as a phased transition in which work, savings, geography and lifestyle all become levers you can adjust to keep your plan resilient and personally meaningful.