Why Your Credit Card Debt Feels So Overwhelming

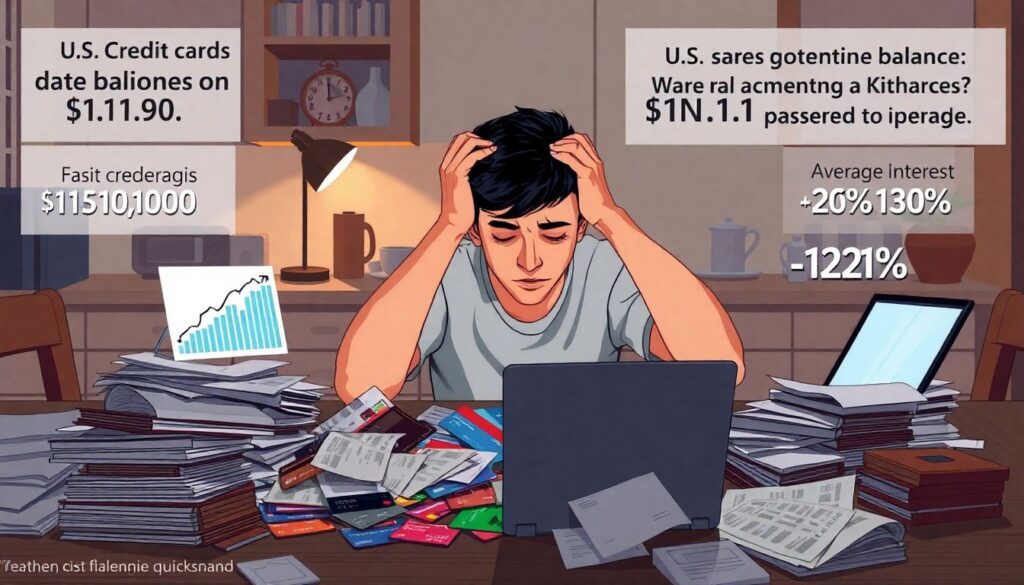

If your credit cards are maxed out and minimum payments keep creeping up, you’re not alone and you’re definitely not “bad with money.” In 2024, U.S. credit card balances passed $1.1 trillion, and average interest rates pushed above 20%. That combo makes even small balances feel like quicksand. The good news: once you organize the chaos, progress can be surprisingly fast. Instead of asking vaguely how to pay off credit card debt fast, you’ll get much better results by building a realistic system: clear numbers, specific targets, and automatic habits that don’t rely on willpower every single month. This step‑by‑step plan is built for real life, not fantasy budgets or extreme frugality that collapses after two weeks.

Step 1: Turn the Mess Into a Clear Picture

Start by pulling every credit card statement or logging into each account. Write down, in one place, the balance, interest rate (APR), minimum payment, and due date. Don’t guess; the numbers usually look better when they’re finally on paper. This snapshot is the base for all the best credit card debt payoff strategies, because you can’t choose a method if you don’t know what you’re working with. Next, total your take‑home income and list all fixed bills: rent, utilities, insurance, basic groceries, transport. Whatever remains is your “debt attack” money. Even if that amount feels tiny, clarity turns nameless anxiety into a concrete plan with real levers you can pull.

Step 2: Pick a Payoff Strategy That Fits Your Personality

There are two classic ways to prioritize cards. The “avalanche” method targets the highest interest rate first, saving you the most money over time. The “snowball” method kills the smallest balance first, giving a quick win and emotional momentum. Both work, so focus on which one you’re more likely to stick with on a bad month. If you’re analytical and patient, avalanche usually wins. If you need to see fast progress or you’re easily discouraged, snowball can be more powerful. The real trick isn’t perfection; it’s consistency. A strategy that feels natural is far more effective than a mathematically ideal plan you abandon after three billing cycles.

Step 3: Build a Simple, Repeatable Monthly System

Now turn your plan into routines so it runs almost on autopilot. Choose one “target card” and send every spare dollar there while paying minimums on the rest. Automate those minimums to avoid late fees and credit score damage, then schedule an extra payment to the target card right after payday, before the money quietly disappears elsewhere. To keep things practical, do a quick 10‑minute money check‑in once a week: verify transactions, confirm you’re on track, and decide whether any small extras (refunds, side gig cash, tax rebates) can go directly to your current target card. Over time, this steady rhythm does more than occasional heroic lump‑sum payments.

Step 4: Use Tools Like Consolidation and Transfers Wisely

If your APRs are sky‑high, it’s worth exploring credit card debt consolidation options, but only with a clear budget in hand. A lower fixed rate personal loan can simplify several cards into one payment, reducing interest if you don’t keep swiping the old cards. Similarly, well‑chosen credit card balance transfer offers can give you a 0% promo period to attack the principal aggressively. The key word is “chosen”: transfer only what you can realistically pay off before the promo expires, and watch out for transfer fees. These tools amplify a solid plan; they don’t replace the need for disciplined spending and steady monthly payments.

Step 5: Find Extra Cash Without Ruining Your Life

To speed things up, you’ll need more “debt attack” money, but that doesn’t require living on instant noodles. Start with easy wins: cancel dead subscriptions, downgrade rarely used services, rethink one or two high‑cost habits like frequent delivery or rideshares. Then look at temporary income boosts: a short‑term side gig, a seasonal job, or selling stuff you don’t use. The goal isn’t perfection; it’s creating a modest but reliable surplus you can send to your target card every month. When you see balances actually dropping, motivation tends to rise, and small sacrifices feel more like short‑term trades than endless deprivation.

Step 6: Use Programs and Protections When Things Are Tight

If you’re already missing payments or getting collection calls, ignoring the situation only makes it worse. Talk to your card issuers about hardship arrangements or reduced interest; they offer these more often than you’d think because they’d rather get paid something than nothing. Nonprofit credit counseling agencies can help you compare debt relief programs for credit card debt, negotiate lower rates, and build a structured repayment plan. Be cautious with any company that promises to “erase” debt quickly or tells you to stop paying your cards altogether; that path can demolish your credit and trigger legal action if you don’t understand the trade‑offs.

The Bigger Picture: Personal Debt and the Economy

Your individual plan sits inside a much larger trend. As rates climbed in recent years, the cost of carrying revolving balances jumped sharply, pulling more household income into interest instead of savings or consumption. That shift has macro effects: when millions of people cut back because of credit card bills, retail sales and travel slow, and businesses feel the drag. On the flip side, as households pay down revolving balances, they free up cash for long‑term goals, which supports more stable economic growth. That’s why economists watch card delinquency data as a signal of growing financial stress in the wider system.

How the Industry Adapts to Changing Debt Patterns

Banks and fintech companies track repayment behavior closely and adjust products based on how people actually manage debt. When more consumers struggle, you tend to see a surge in balance transfer cards, refinancing products, and mobile tools that nudge on‑time payments. Competitive pressure pushes issuers to refine rewards, but also to tighten underwriting when risks rise. Over time, widespread use of the best credit card debt payoff strategies—like automation, targeted attacks, and smarter refinancing—can push the industry to offer clearer pricing and more transparent terms. If borrowers keep demanding fairer credit card debt consolidation options and more predictable interest structures, providers eventually follow the money.

Putting It All Together: Your Action Plan

1. List every card with balance, APR, minimum, and due date.

2. Calculate your true “debt attack” amount after essentials.

3. Choose avalanche or snowball and pick your first target card.

4. Automate minimums; schedule extra payments right after payday.

5. Consider consolidation or transfers only after your budget is clear.

6. Hunt for realistic savings and short‑term income boosts.

7. Get help early if payments are already past due.

Following this sequence turns a vague desire to get out of debt into a concrete, step‑by‑step roadmap. Your income, your numbers, and your timeline are unique, but the structure stays the same—and that structure is what slowly moves you from overwhelmed to organized.

Комментарии