Understanding the Unique Retirement Needs of Remote Workers

The rise of remote work has revolutionized how people earn a living, but it also introduces unique challenges in retirement planning. While flexibility and location independence are attractive benefits, remote workers—especially freelancers, contractors, and digital nomads—often lack traditional employer-sponsored retirement plans. This means they must take a more proactive approach to secure their financial future.

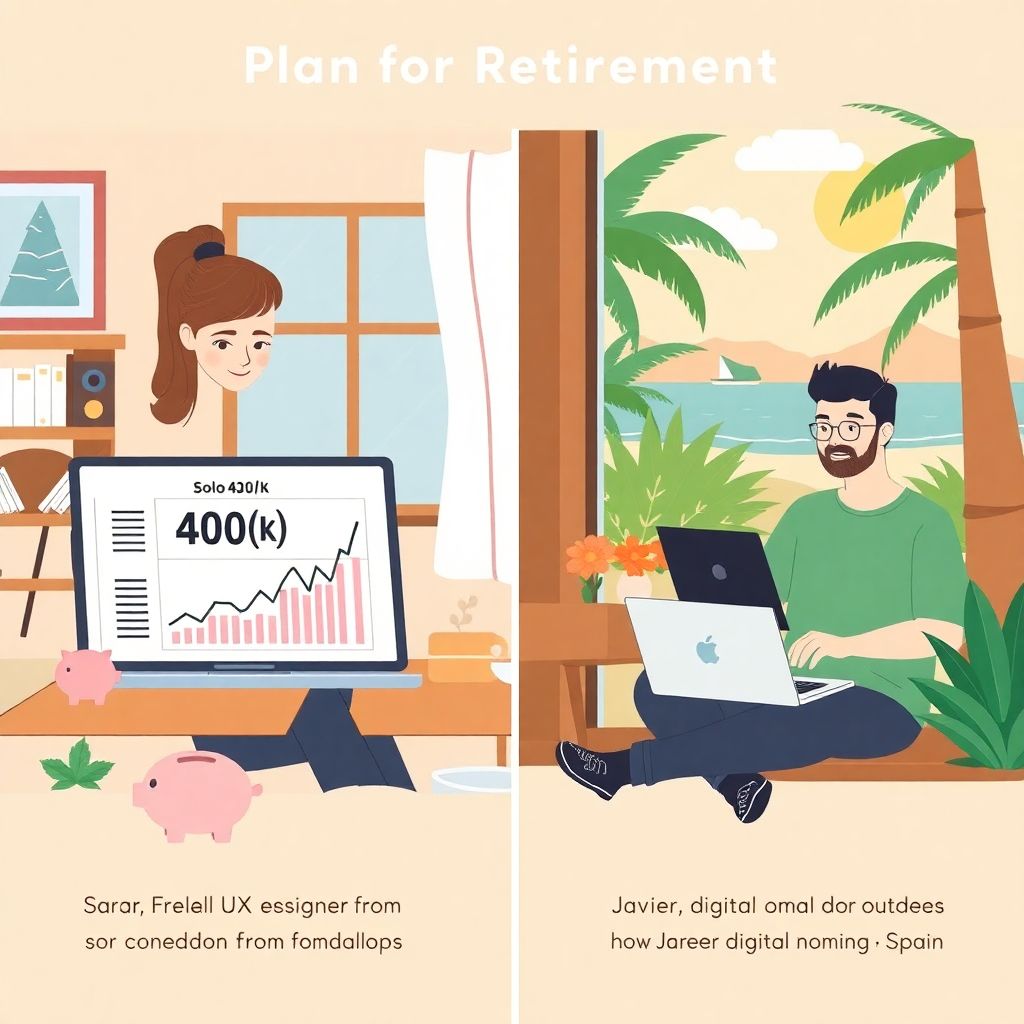

For example, Sarah, a freelance UX designer from Colorado, transitioned to remote work in 2018. Without a 401(k) or employer match, she realized she needed to build her own retirement infrastructure. Her journey highlights the importance of self-directed retirement strategies for remote professionals.

Why Remote Workers Must Plan Differently

Unlike traditional employees, remote workers may juggle multiple income sources, irregular cash flow, and a lack of access to employer benefits. These factors make consistent retirement saving more complex but no less critical.

Challenges Remote Workers Commonly Face:

– No automatic savings mechanisms: Without payroll deductions, saving for retirement must be a conscious decision each month.

– Fluctuating income: Freelancers and gig workers experience income variability, complicating long-term planning.

– Lack of employer match: Many remote workers miss out on “free money” from employer contributions to 401(k) or pension plans.

The key difference is that remote workers must act as both employee and employer in their retirement strategy—managing contributions, setting goals, and maintaining discipline.

Practical Retirement Planning Strategies

1. Choose the Right Retirement Account

Remote workers in the U.S. have several tax-advantaged retirement account options. Selecting the right one depends on income level, business structure, and long-term goals.

Technical Block: U.S. Retirement Account Options

– Traditional IRA: Contribute up to $6,500 in 2023 ($7,500 if over 50). Pre-tax contributions lower your taxable income.

– Roth IRA: Same contribution limits as Traditional IRA but funded with after-tax dollars. Qualified withdrawals in retirement are tax-free.

– Solo 401(k): Ideal for self-employed individuals with no employees. Allows contributions up to $66,000 in 2023 (including employer and employee portions).

– SEP IRA: Easy-to-manage option for freelancers. Allows up to 25% of income, capped at $66,000 in 2023.

Sarah, the UX designer, chose a Solo 401(k) and set up auto-contributions of 20% of her monthly income. This helped her build over $45,000 in retirement savings within three years.

2. Set a Savings Target

Remote workers often underestimate how much they’ll need in retirement. A common rule of thumb is to aim for 70–80% of your pre-retirement income annually.

How to Estimate Retirement Needs:

– Multiply your expected annual expenses in retirement by 25 to get a rough savings goal.

– Use online retirement calculators tailored for self-employed workers.

– Adjust for inflation, healthcare, and travel—common desires in retirement.

For instance, if you expect to need $40,000 per year, you’ll need about $1 million saved under the 4% safe withdrawal rule.

3. Automate and Diversify

Without payroll deduction, automation is crucial. Set up recurring transfers to your IRA or Solo 401(k) shortly after your invoices are paid.

Smart Habits for Long-Term Success:

– Automate 15–20% of income into retirement accounts.

– Reinvest tax refunds or windfalls into your nest egg.

– Diversify with a mix of stocks, bonds, and real estate ETFs.

Diversification reduces risk, especially for remote workers whose income streams may also be volatile. A conservative mix may include 60% equities, 30% bonds, and 10% alternative assets.

Don’t Forget Taxes and Health Coverage

One often overlooked aspect is how retirement withdrawals will be taxed. Roth IRAs offer tax-free withdraws, while Traditional IRAs and Solo 401(k)s are taxed as ordinary income. Be strategic based on your current and expected tax brackets.

Another concern is healthcare post-retirement. Remote workers don’t have employer coverage by default, so they should consider Health Savings Accounts (HSAs), which offer triple tax advantages and can be used for medical expenses in retirement.

HSA Benefits:

– Contributions are tax-deductible.

– Growth is tax-deferred.

– Withdrawals for qualified medical expenses are tax-free.

Real-Life Case: Building a Retirement Plan While Traveling

Javier, a digital marketing consultant from Spain, works remotely while traveling through Latin America. He earns about $90,000/year but operates without a home base. To stay retirement-ready, he:

– Opened a Roth IRA in the U.S. through a brokerage that accepts foreign addresses.

– Invests 20% of his income monthly, regardless of currency fluctuations.

– Keeps a separate emergency fund in a high-yield savings account to avoid early retirement account withdrawals.

Javier’s strategy allows him to enjoy the digital nomad lifestyle without sacrificing his future financial security.

Final Thoughts

Retirement planning for remote workers demands intention, flexibility, and self-discipline. While it may lack the structure of traditional employment benefits, the autonomy of remote work gives you the power to tailor a plan that fits your lifestyle.

With the right tools—automated savings, strategic account choices, diversified investments—you can build a secure retirement no matter where you work from. Whether you’re coding on a beach in Bali or consulting from a cabin in Vermont, your future self will thank you for starting today.