Why Negotiating Your Interest Rate Is Absolutely Worth It

Most people quietly pay what the bank tells them and never even try to negotiate lower interest rate on credit card or loan products. Но lenders actually change rates all the time — they just usually do it for people who ask. Even a small cut, say from 24% to 18%, can shave months off repayment and save hundreds of dollars. Think of it like haggling on a car price, только цифры другие. The bank’s first offer is rarely the final one; it’s just the starting point. Your job is not to complain, but to calmly show why you deserve better terms and make it easy for the lender to say “yes” instead of “we’ll keep it as is.”

Necessary Tools Before You Pick Up the Phone

You don’t need a finance degree, but you do need данные под рукой. First, download your last 6–12 months of statements for all cards and loans. Note your current APR, minimum payments, and any late fees. Second, check your credit score using a free service; screenshot or print it. Third, look up competing offers: new card promos, balance transfer deals, and personal loan rates from online lenders. This gives you leverage. Finally, prepare a simple one-page cheat sheet with bullet points: income, employment stability, payment history, and offers from other banks. Having this in front of you keeps your voice steady and your arguments четкими when you start any credit card interest rate reduction negotiation tips call.

Step-by-Step: How to Lower APR on Credit Cards and Personal Loans

1. Do a Quick Financial X-Ray

Before you even think about how to lower apr on credit cards and personal loans, разложи всё по полочкам. Write down every balance, current rate, and how much you actually can pay each month without starving yourself. This isn’t just for you — it’s ammunition. When a bank hears, “I’m paying $350 across three cards, I’ve never missed a payment, and I’d like to stay with you long term,” you sound organized and serious. That alone sets you apart from the usual “I’m broke, help” calls that support teams hear daily and makes a constructive conversation намного вероятнее.

2. Script Your Pitch Like a Short Sales Call

Most people improvise and then freeze. Instead, write down a short, человеческий script. Example: “I’ve been a customer for five years, never missed a payment, and my credit score improved to 720. I’d like to keep using this card, but the APR is high. Can you review my account and see if I qualify for a lower rate?” This works both for cards and when thinking about how to ask bank to lower interest rate on loan. Practice it out loud twice; you’ll sound calmer and more confident. Keep the tone friendly but firm, as if you’re negotiating a salary, not begging for a favor.

3. Call the Right People, in the Right Order

Don’t just mash the generic hotline. Call, ask for “account retention” or “customer loyalty department” — these teams often have more flexibility. Start with your oldest card or loan, where you have the longest relationship and strongest история платежей. If the first agent says they “can’t do anything,” politely ask to speak with a supervisor. Same with personal loans: front‑line agents follow scripts, but supervisors may have special offers or “discretionary adjustments” they can apply. If you strike out in one call, wait a day and try again; you might land on a more accommodating employee who sees your case иначе and is willing to help.

4. Use Creative Leverage, Not Empty Threats

Instead of yelling, use quiet pressure. Mention that you received pre‑approved offers with lower rates or a balance transfer card and you’d prefer to stay if they can be competitive. For the best ways to reduce interest on personal loan, get an actual quote from a reputable online lender first; then say, “Another lender offered me X%, can you match or at least come closer?” You’re not threatening to leave blindly; you’re showing real options. Lenders hate losing good payers, so a documented outside offer can gently push them to stretch their internal rules in your favor without escalating конфликт.

Non-Standard Tactics Most People Never Try

Один из нестандартных ходов — предлагать взаимную выгоду. For example, ask for a lower rate in exchange for setting up automatic payments or agreeing to a slightly higher fixed monthly payment. Frame it as risk reduction for the bank. Another trick: ask for a temporary rate reduction for 6–12 months instead of a permanent cut. It’s easier for them to approve, and you still win valuable time. You can also request removal of recent penalty APRs if you had a one‑off late payment and a solid history before that. The key is to negotiate something конкретное, not just “can you help me somehow?”

Turning Multiple Debts into a Negotiation Weapon

If you have several products with one bank — say a checking account, a credit card, and a personal loan — используйте это как пакет. Call and position yourself as a “relationship client”: “I have my salary coming into your bank, and I hold both a loan and a card with you. I’d like to review the overall cost, starting with interest rates.” Then ask whether they have a bundled offer or VIP program that could give you better terms. Banks are more flexible when they see the total revenue you bring. You’re basically saying: “I can consolidate everything with you — or somewhere else. What can you do so it’s выгодно обоим?”

Troubleshooting: When the Answer Is “No”

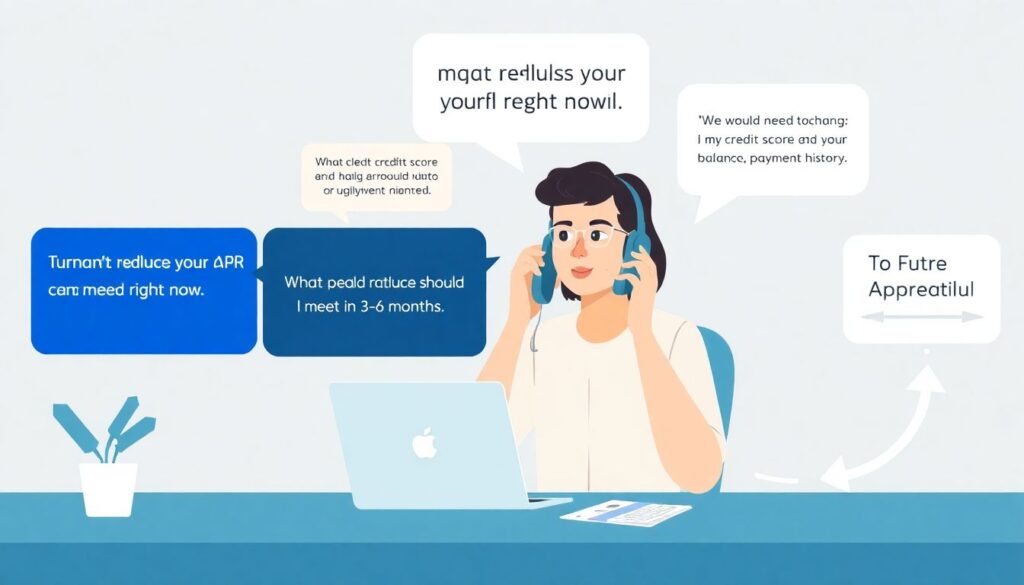

If They Refuse to Lower Your Rate

Иногда you’ll get a firm “we can’t reduce your APR right now.” Don’t stop there. Ask what exactly would need to change: “Is it my credit score, my balance, or payment history? What specific criteria should I meet to qualify in 3–6 months?” This turns a dead end into a roadmap. You can also pivot: request a reduced rate for new purchases only, or for the next 6 months, or ask them to waive a fee or give a statement credit. Even if you lose the rate battle today, you can still win smaller concessions that cut your overall cost of borrowing заметно.

Alternative Moves If Negotiations Fail

Когда все в лоб не работает, go sideways. Consider a 0% balance transfer card and move only part of the debt first, using it as proof you’re serious. Apply for a lower‑rate personal loan from a credit union or fintech and use it to refinance high‑interest cards. That alone often solves how to lower apr on credit cards and personal loans in practice, even if your original bank wouldn’t budge. Just watch the fees and avoid stretching the term so much that you pay more overall. And remember: once you refinance, call your old lender again — suddenly, they may “find” options that were mysteriously unavailable раньше.

When You Shouldn’t Push Too Hard

If your credit is shaky, you’re behind on payments, or just started a new job, агрессивный торг может навредить. Pushing for a rate cut might trigger a review that exposes risks and nudges them to tighten your limit instead. In that case, focus first on stabilizing payments: avoid new debt, set up autopay for at least the minimum, and build three on-time payments in a row. Then circle back and ask again with a better story to tell. Negotiation is not a one‑time event; it’s a series of nudges in the right direction as your numbers постепенно улучшаются.

Locking In Gains and Building Long-Term Leverage

Каждый раз, когда вам идут навстречу, закрепляйте успех. Ask the agent to confirm the new APR, duration, and any conditions via email or in your online banking messages, then screenshot everything. Update your debt spreadsheet so you actually see the win — that visual reminder motivates you to keep going. Over time, your growing track record of responsible behavior turns into a powerful argument for future talks. Once you’ve done a few successful calls, negotiating a lower rate will feel less like a scary confrontation and more like a routine maintenance task — just another smart move in managing your money, not нервный подвиг.