Why Retirement Planning by Age Matters More Than Ever

Retirement planning by age 20s 30s 40s 50s isn’t just a catchy phrase; it reflects how your priorities actually change as you move through life. Your 25‑year‑old self and your 55‑year‑old self face completely different financial realities, and your strategy has to evolve with you.

Over the last three years, the gap between people who save early and those who don’t has widened. Fidelity’s 2023 data shows average 401(k) balances around:

– Early 20s: ~$16,000

– 30s: ~$45,000

– 40s: ~$120,000

– 50s: ~$180,000

At the same time, the U.S. Federal Reserve’s 2023 report on household well‑being found that roughly 30% of non‑retired adults still have no retirement savings at all. That contrast is why starting where you are — right now — is critical.

—

A Quick Historical Snapshot: How Retirement Got So Complicated

For most of the 20th century, retirees in many developed countries leaned on three legs: a government pension (like Social Security), a company pension, and a bit of personal savings. Your employer often promised a fixed payout for life. Planning was simpler; the company did the math.

From the 1980s onward, a big shift happened:

Defined‑benefit pensions (the “we’ll pay you for life” kind) started fading, and defined‑contribution plans (401(k), 403(b), workplace plans, IRAs) became dominant. Now you decide how much to contribute, what to invest in, and how to withdraw later.

Over the last 3–5 years, this shift has solidified:

– Vanguard’s “How America Saves 2023” showed over 100 million Americans participating in defined‑contribution plans.

– Automatic enrollment features, added more widely since around 2019, helped younger workers start earlier — but contribution rates are often still too low to sustain a comfortable retirement.

In short: the responsibility for your future income has moved from your employer to you. That’s why getting clear on your decade‑by‑decade strategy matters.

—

Core Principles That Don’t Change With Age

Before we break it down by decade, a few basic rules apply to almost everyone:

1. Start as early as possible.

Time in the market matters more than timing the market. A 25‑year‑old saving $300/month at 7% can end up with roughly double the retirement balance of a 40‑year‑old saving the same amount.

2. Increase your savings rate regularly.

Each raise or bonus is a chance to bump your retirement contributions by 1–2% instead of upgrading your lifestyle.

3. Use tax‑advantaged accounts first.

401(k), 403(b), IRA, Roth IRA and similar local equivalents are usually your best retirement plans for young adults in their 20s and 30s, and they stay relevant later too.

4. Diversify and ignore short‑term noise.

A simple mix of low‑cost index funds often beats constant trading. Over the last 3 years — despite volatility in 2022 and 2023 — long‑term investors who stayed the course generally recovered better than those who tried to time every dip.

5. Plan for longevity.

Life expectancy keeps edging up. A 30‑year‑old today may easily need to fund 25–30 years of retirement; that changes how much you need to save.

—

Using Tools: Make the Math Easy on Yourself

Instead of guessing, plug your numbers into a retirement savings calculator by age. Many brokerages and financial sites have free tools where you input:

– Current age

– Income

– Current savings

– Monthly contributions

Then you see whether you’re on track. Re‑run the calculator once a year or after big changes in income, family, or location. Think of it like your financial annual check‑up.

—

Your 20s: Build Habits, Not Perfection

What to Focus On

In your 20s, the dollar amounts matter less than the habits. Your main job is to:

– Start

– Automate

– Learn the basics

Even if you’re paying off student loans or building an emergency fund, you can usually carve out 5–10% of your income for retirement if you’re intentional.

If your employer offers a 401(k) match, make that your bare minimum. For example, if they match 4% of your salary, contribute at least 4%. Otherwise, you’re literally leaving free money on the table.

How Much Should You Aim For?

By late 20s, a common (not mandatory) guideline is:

– Have 0.5–1× your annual salary saved for retirement

If you’re not there, don’t panic. The important move is to increase your savings rate as your income rises. Over the last three years, starting contribution rates for auto‑enrolled young adults have often been set at just 3%. That’s usually too low; try to move to 10–15% total (you + employer) as early as you can.

Practical Example in Your 20s

Imagine you make $40,000 at 25 and start contributing:

– 10% to your 401(k) = $4,000/year

– Employer matches 4% = $1,600/year

At a 7% average return, by age 35 you could have around $75,000–$80,000 without ever doing anything fancy. That’s the power of starting early.

Common Misconceptions in Your 20s

– “I’ll save more when I earn more.”

Reality check: Lifestyle creep eats raises. People who say this often spend more, not save more.

– “Investing is only for rich people.”

Not anymore. Over the last 3 years, many brokerages eliminated trading commissions and minimums. You can start with $50–$100.

– “I’m too young to worry about retirement.”

That attitude is why the Fed’s 2023 data shows millennials and Gen Z lagging behind recommended savings benchmarks. Your 20s are your secret weapon.

—

Your 30s: Scale Up and Get Strategic

What Changes in Your 30s

Careers get more stable, incomes (usually) grow, and responsibilities appear: mortgages, kids, aging parents. The upside? You probably have more income flexibility than ever before.

This is when people often ask: “how much should I save for retirement at 30 40 50?” For your 30s specifically, many planners suggest aiming to save 15–20% of your gross income toward retirement (including employer match).

By age 35, a common benchmark is:

– 1–2× your annual salary saved

By age 40:

– 2–3× your salary

Best Retirement Plans for Young Adults in Their 20s and 30s

In this stage, you’re usually juggling:

– Workplace plans (401(k), 403(b), etc.)

– IRAs (traditional or Roth)

– Maybe a taxable brokerage account once you max out tax‑advantaged options

For many, the best retirement plans for young adults in their 20s and 30s still remain employer‑sponsored accounts plus a Roth IRA, especially if you expect your income to grow and tax rates to be higher later.

Example: A 35‑Year‑Old Reset

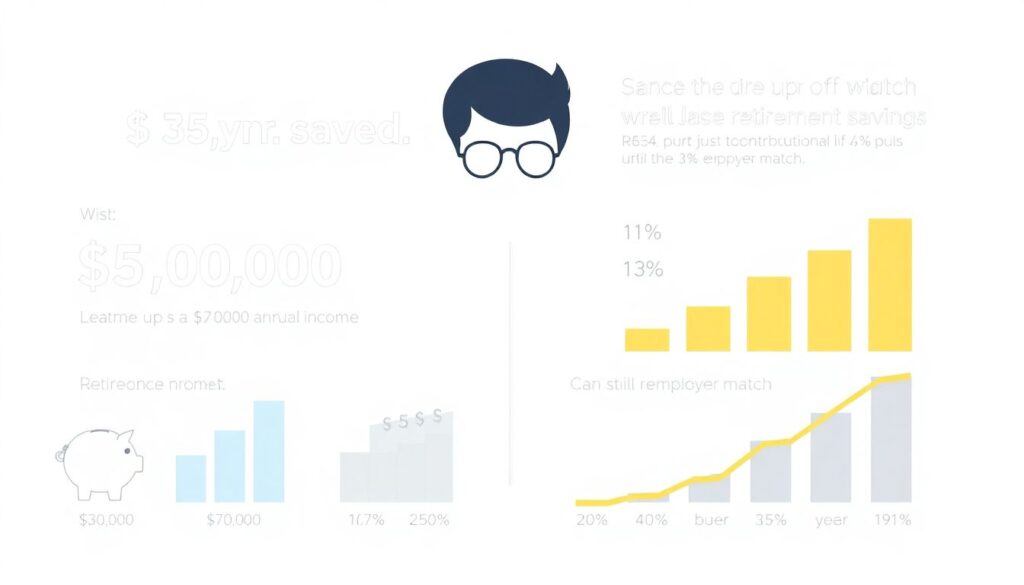

Let’s say you’re 35 with:

– $30,000 saved

– $70,000 annual income

– Contributing 6% to your 401(k) with a 3% match

If you increase your contribution by just 1% each year until you hit 15% (plus employer 3%), you can still catch up. Running this through a retirement calculator shows you can potentially hit a seven‑figure balance by your late 60s, even if you started slow.

Misconceptions in Your 30s

– “Buying a house is my retirement plan.”

A home can be an asset, but it doesn’t automatically produce cash flow in retirement. You still need actual investment accounts.

– “I can pause retirement savings while the kids are young.”

Many parents do this and then struggle to catch up. College can be funded with scholarships and loans; retirement can’t.

– “I’ve missed the window; starting now won’t matter.”

Wrong. According to Vanguard’s 2024 data, people who started serious saving in their mid‑30s but kept contributions high still built solid retirement balances by their 60s.

—

Your 40s: Catch‑Up, Course‑Correct, and Reduce Risky Gaps

The Reality Check Decade

Your 40s often feel like “peak juggling”: older kids, aging parents, peak career pressure. This is also the decade where many people finally look at their numbers and either breathe a little easier or panic.

The good news: with 20+ years until retirement, you still have time for powerful course corrections.

By age 45, typical benchmarks:

– Aim for 3–4× your salary saved

By age 50:

– Around 4–6× your salary

If you’re behind, you’re not alone. Recent surveys between 2022 and 2024 consistently show that a majority of Gen X feel “not on track” for retirement — but many also increased their savings rate after using a calculator or talking to an advisor.

How Much Should I Save for Retirement at 40?

If you’re in your early to mid‑40s and underfunded, target:

– 20% or more of income toward retirement if possible

This might mean:

– Maximizing 401(k) or equivalent

– Adding an IRA if eligible

– Using bonuses or side‑income solely for investing

Example: A 45‑Year‑Old Catch‑Up Strategy

Suppose you’re 45 with:

– $150,000 saved

– $100,000 income

If you start contributing the maximum allowed to your retirement plan each year (including catch‑up contributions as you hit 50), and maintain a balanced portfolio, you still have a realistic path to a respectable retirement. Over 20 years at a 6–7% average return, that combination of new contributions and growth can close a surprising amount of the gap.

Misconceptions in Your 40s

– “The stock market is too risky now; I should go all‑in on cash.”

Over the last 3 years, cash yields have been higher than they were in the 2010s, but historically, long‑term inflation still eats away at cash. You usually need some stock exposure for growth.

– “I’ll just work forever.”

Surveys from 2022–2024 show many people plan to work past 65, but actual retirement ages are often lower due to health, layoffs, or caregiving needs. Counting on “working forever” is a risky plan.

—

Your 50s: Lock In, Optimize, and Stress‑Test the Plan

What Your 50s Are Really About

In your 50s, you’re in the “make it or fix it” zone. Retirement is no longer theoretical; it’s coming into view.

Key priorities:

– Maximize contributions (use catch‑up rules)

– Refine your investment mix

– Start planning *how* you’ll draw income, not just *how much* you’ll have

How Much Should I Save for Retirement at 50?

By your early 50s, planners often suggest:

– 6–8× your salary saved by 55

– 8–10× your salary by your late 50s

If you’re not close, don’t freeze. The combination of higher catch‑up contribution limits (which have increased over the last few years) and a few extra working years can meaningfully improve your outlook.

Example: A 52‑Year‑Old Reboot

You’re 52 with:

– $350,000 saved

– $90,000 income

You:

1. Max out your workplace plan, including 50+ catch‑up contributions.

2. Shift your portfolio to slightly lower volatility but still growth‑oriented.

3. Use a retirement calculator once a year to test different retirement ages (65, 67, 70).

You may find that retiring at 67 instead of 62 plus higher savings now can mean hundreds of thousands more in your nest egg.

Misconceptions in Your 50s

– “It’s too late to change anything.”

Not true. Research from major providers in 2022–2024 shows that people who seriously ramped up savings in their 50s still significantly improved their replacement income in retirement.

– “I must become ultra‑conservative now.”

You may live another 30–40 years. Going 100% bonds or cash at 55 can increase the risk that you outlive your money.

—

Frequent Myths Across All Ages

Let’s quickly bust a few persistent myths that keep people stuck:

1. “Social Security (or my country’s state pension) will cover it.”

In the U.S., Social Security replacement rates for average earners are often around 30–40% of pre‑retirement income. Most people need around 70–80% to feel comfortable. Other countries’ systems vary, but few replace your full income.

2. “If the market is down, I should stop contributing.”

Over the short term, markets are noisy. Over 20–30 years, historically, downturns end up looking like blips — and downturns are actually when you’re buying investments at a discount.

3. “All debt must be gone before I invest.”

High‑interest debt (like 20% credit cards) should absolutely be attacked fast. But delaying all retirement savings until you’re completely debt‑free usually means losing valuable compound growth.

4. “A financial advisor is only for the wealthy.”

Many advisors now offer hourly or flat‑fee planning, and robo‑advisors have low minimums. Searching for a financial advisor for retirement planning near me or using a reputable online platform can connect you with help faster than you think.

—

A Simple Step‑By‑Step Plan to Start Today

No matter your age, you can follow this basic framework:

1. Get the numbers.

Calculate net worth, current retirement balances, and monthly savings rate.

2. Use a retirement calculator.

Run a retirement savings calculator by age using your specific data to see if you’re on track.

3. Set a new savings target.

Decide on a realistic percentage to contribute now. Plan small increases every 6–12 months.

4. Automate everything.

Automatic payroll deductions or transfers to retirement accounts so you don’t rely on willpower.

5. Review once a year.

Re‑check contributions, rebalance your portfolio, and re‑run your projections.

—

Final Thoughts: Start Where You Are, Not Where You “Should” Be

You can’t rewind to your 20s, but you also don’t need a perfect past to build a solid future. The past three years of data are blunt: people who systematically save and invest — at any age — end up dramatically better prepared than those who wait for “the right time.”

– In your 20s: start and learn

– In your 30s: scale up and get intentional

– In your 40s: course‑correct and catch up

– In your 50s: optimize and stress‑test

Pick the decade you’re in, apply the steps that fit, and commit to one specific action this month — whether it’s upping your contribution by 1%, opening your first IRA, or booking a meeting with an advisor.

Your future self, at 65 or 70, will be incredibly glad you didn’t wait.